When you open a new bank account, one of your first documents received will be a bank statement. A bank statement is a document you receive every quarter or month that summarizes your activity showing what money went in and out of a bank account. It can help you track finances, catch account mistakes, and understand your spending habits on a regular basis.

The statement includes an account summary, transaction details, and instructions for reporting any inaccuracies. If you have checking and savings at the same bank, you might get both in the same report. A statement period is usually one month long, and it may not match up with the calendar month.

Most of us don’t actually look at it too in depth unless something’s wrong. You may take a quick glance at your balance every month, but chances are that piece of paper goes straight in the trash shortly after.

However, if you read it correctly, your statement can tell much more than you may realize. You can find financial habits, highlight potential problems, and prove your worthiness as a borrower. You can also build a detailed budget using your bank statement.

How To Read A Bank Statement

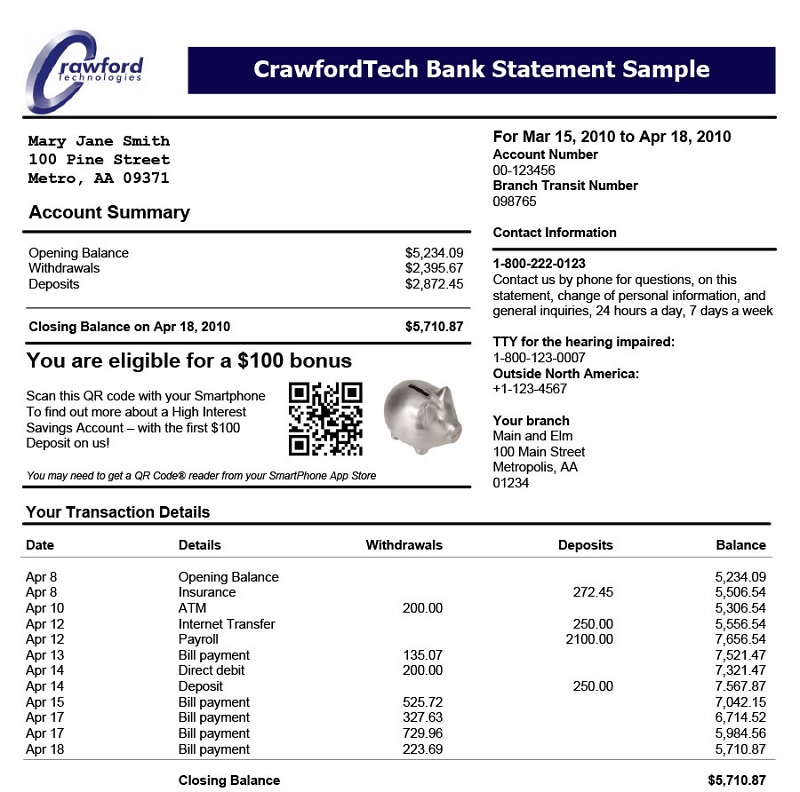

Your bank statement shows your transactions from a checking or savings account over a certain statement period.

Each statement’s summary generally contains these basic sections:

- The starting account balance

- Your deposits (direct deposits, checks cashed, transfers received)

- Your withdrawals (purchases, transfers sent, ATM withdrawals)

- Any interest the account earned

- Any fees charged by the bank

- The new account balance

Use bank statements to monitor your spending and your deposits. In addition, a mortgage lender might also ask to see your bank statements to make sure you have enough to make monthly payments or to ensure that no suspicious deposits have occurred recently.

Important Terms To Know

If you’ve never really checked your bank statement, you may not know all the terms. Thankfully, understanding a bank statement is simple once you learn what each part represents. Here are the most important terms to know:

- Starting balance: This is the amount you had in your account during the beginning of the statement period before any deposits or withdrawals were made.

- Ending balance: This is the amount in your account when the statement period ends. If you save more money than you spend, your ending balance will be higher than the starting balance. If you spend more or transfer more to a different account, you’ll have a lower ending balance than you started with.

- Statement period: These are the dates during which the transactions occur, usually a month-long period. However, if the statement says, “January 2019,” that doesn’t necessarily mean the statement period was for the month of January. It may begin at the end of December and end a few days before the end of January.

- Deposits: These are individual installments of funds into your account. This can include direct deposit from your employer, cashed checks, wire transfers, money you transferred from PayPal or Venmo, and other credits.

- Withdrawals: This shows the transactions where you withdrew funds from your account. It can include both online transfers, like a payment to your credit card, and transactions that occurred with your debit card.

- Interest: If you earned interest during the period, your bank statement will show how much you earned. Some checking accounts earn interest like the Chase Premier Plus Checking account. If you have multiple savings accounts under the same umbrella account, you may see the total interest paid and the total interest for each account. You may also find the amount of interest you’ve earned over the life of the account.

- Fees: You can find the exact fees you paid during the statement period. This can include overdraft fees, returned check fees, ATM withdrawal fees, and a monthly maintenance fee. If you used your debit card out of the U.S., you may have been charged a foreign transaction fee or ATM withdrawal fee.

- Daily balance detail: Your bank may also show your balance for each day of the statement period. You can see how your balance fluctuated throughout the month. It’s useful for those who like examining detailed spending habits.

- Overdraft protection: You may have overdraft coverage on your account. This is known as an insufficient funds fee. Banks charge overdraft fees when you write a check or use your debit card for an amount that exceeds your account balance. You can check whether it had to kick in at any point during the statement period.

How to Use Your Bank Statement

Know how to use your bank statement properly to further help your financial goals. Each time you get a new statement, do these three things:

1. Reconcile Your Accounts

Regularly review your bank statements to make sure the bank calculated everything correctly. Match up your own record of deposits, withdrawals, interest and fees with the information on your bank statement. This’ll help you catch any mistakes or even fraud. It can also help you avoid overdraft fees if the bank statement shows that you have less money than you think.

2. Correct Any Errors

Keep an eye out for any errors when checking your bank statement, like transaction amounts you don’t think are accurate or a mistakenly charged fee. The bank has many people using their services, so it’s unlikely they’ll be as attentive about your account as you are. Therefore, you’re responsible for noticing any mistakes.

It’s usually only possible to correct mistakes with your bank within a certain period of time. Generally, it’s 60 days. Thus, you should review your statement upon receiving it. If something seems off, call your bank’s customer service line immediately.

3. Keep A Record

By law, banks have to keep your statements available for five years. Nonetheless, you should keep your bank statements in a safe place like an online cloud platform or a file cabinet. You can save bank statements as PDFs or scan in your paper statements.

You’ll most likely need to refer to a bank statement when you file your tax return. In addition, if you plan to refinance or buy a home in the near future, potential lenders might want to see several statements.

Author’s Verdict

Bank statements are a great tool to help you track your money and stay on the same page as your bank or credit union. All the information shown in your bank statement are useful for tracking your spending, creating a budget, and reaching your financial goals.

If you don’t have a bank account yet, view our list of checking account promotions and savings account rates to find an account that suits your needs. Once you open an account, feel free to bookmark and refer back to this page to find everything you need.

| PROMOTIONAL LINK | OFFER | REVIEW |

| HSBC Premier Checking Member FDIC | Up to $5,000 Cash | Review |

| U.S. Bank Smartly® Checking | Up to $450 Cash | Review |

| Chase Private Client | $3,000 Cash | Review |

| Chase Business Complete Checking® | $500 Cash | Review |

| Chase Total Checking® | $400 Cash | Review |

| Chase High School CheckingSM | $125 Cash | Review |

| Chase Secure BankingSM | $175 Cash | Review |

| SoFi Checking and Savings Account | $425 Cash | Review |

| Huntington Bank Unlimited Plus Business Checking | $1,000 Cash | Review |

| Huntington Bank Unlimited Business Checking | $400 Cash | Review |

| Axos Basic Business Checking | $200 Cash | Review |

| Axos Bank Business Premium Savings | $600 Cash | Review |

Leave a Reply